[UltraVid id=1 ]

Mortgage 101 – What is a mortgage?

A mortgage loan to finance the purchase of your home consists of five parts.

- Collateral

- Principal

- Interest payments

- Taxes

- Insurance

When you agree to a mortgage you enter into a legal contract promising to repay the loan plus interest and other costs.

Your home is collateral for that loan, if you fail to repay the debt the lender has the right to take back the property and sell it through a process called foreclosure.

The principle is the amount of money borrowed to buy a home. You can put down a percentage of the home’s purchase price, called a down payment, to lower your loans principal amount. Lenders offer a wide range of down payment options so it’s best to ask which one makes the most sense for you and your budget.

Interest is what a lender charges to use the money you borrowed, this amount is usually expressed as a percentage called the interest rate.

Principal and interest make up the bulk of your monthly payments in a process called amortization. Amortization reduces your debt over a fixed period of time.

Your mortgage payment will also likely include taxes that are collected by the local community based on the percentage of the value of your home. These taxes usually go towards things like schools, roads and public services.

Finally, lenders will also require you to purchase home insurance to cover your home against losses from fire, theft, bad weather and other causes. Additional types of insurance may be required depending on the location of your home and the type of loan you choose. They include flood insurance, private mortgage insurance or PMI and mortgage insurance for loans backed by the Federal Housing Administration.

Finally, when choosing a mortgage you may have the option to use positive or negative mortgage points which can alter your interest rate and closing costs. Positive mortgage points are paid as an upfront fee at closing and can help lower your interest rate. Applying negative points to a mortgage increases your interest rate but may reduce closing costs.

Now that you’ve got the fundamentals down keep in mind that lenders offer a wide range of loan products so make sure to ask which broad can work best for you.

If you have mortgage questions please don’t hesitate to contact us.

Other articles that may interest you:

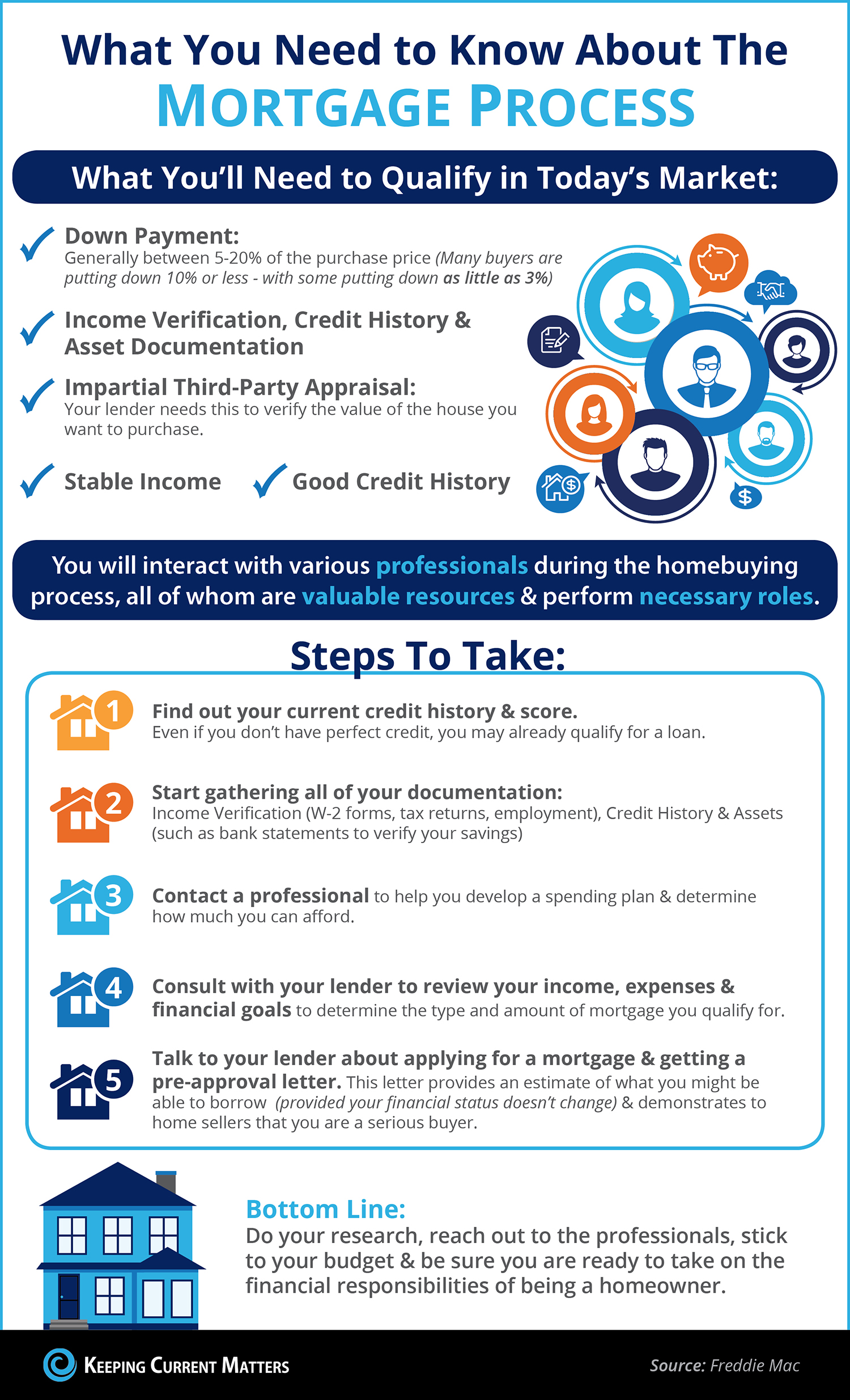

The mortgage process & what you need to know

Home buying in six steps

Don’t get caught in the rental trap

Leave A Comment

You must be logged in to post a comment.